HDFC Fund Manager Addressed Your Questions On India

What our customers in Australia and New Zealand asked Ashish, Senior Fund Manager at HDFC AMC, and the answers that surprised the room.

Kiwi & Australian NRIs Are Different From Other NRIs

We now serve over 15,000 customers across Australia and New Zealand, and if there's one thing all of you have taught us, it's this:

You are not like any other NRI.

The AUD/NZD moves differently. And your instincts about money are different too.

Where investors in the US tend to be more risk-on, investors in Australia and New Zealand are more practical and lean toward the long game: superannuation, KiwiSaver, real estate, things you hold for decades rather than trade.

This means you have a different set of questions that need to be addressed.

Indus is here to provide access to India's growth story, but also the education and context needed to invest responsibly.

That's why we were excited to bring you our webinar, which provided direct access to HDFC's Senior Fund Manager, Ashish Jagnani, and let you put your own questions to him and get direct, unfiltered answers back.

The Four Main Questions That Were Put Forth to Mr. Ashish Jagnani

Before the session, we collected the questions you sent in and Jai Goradia (Indus Founder & CEO) put them forward to Mr. Ashish Jagnani. Four themes surfaced again and again:

Will the falling rupee cancel my returns?

Is India overpriced vs local real estate, US or other markets?

How risky is the current global climate?

What about tax, here and in India?

Q1) Will The Rupee Erase My Returns?

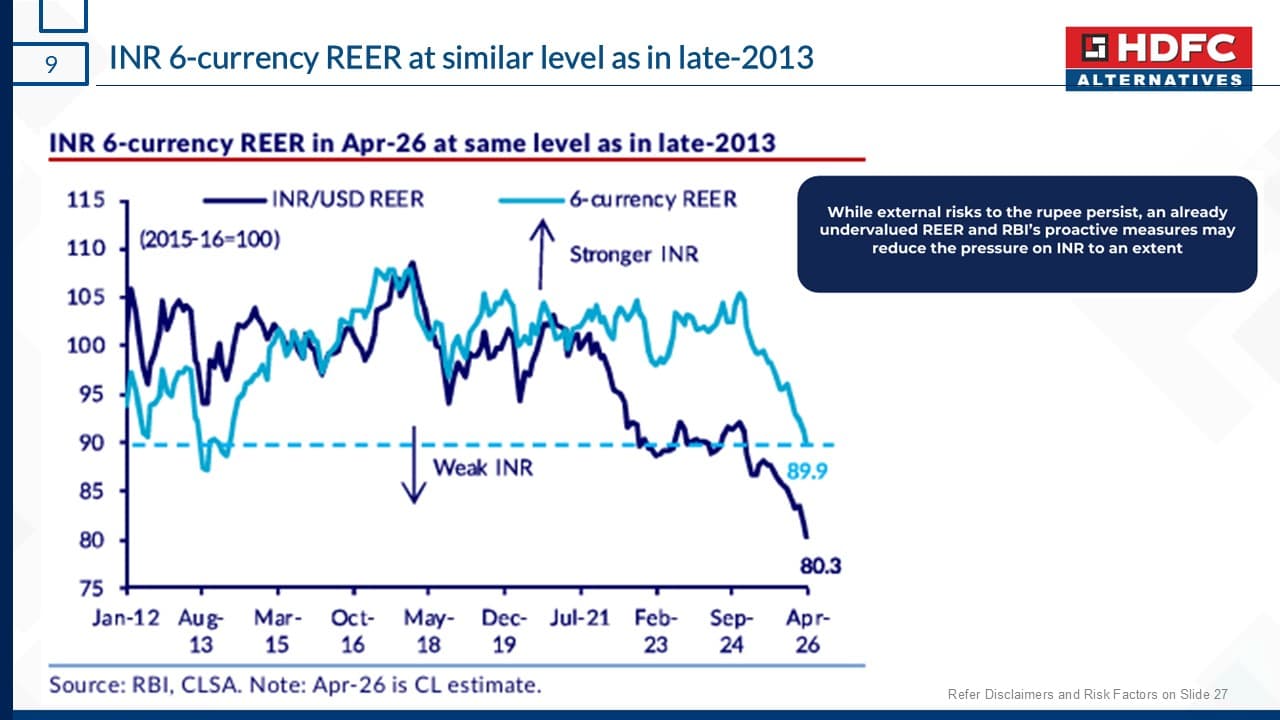

Ashish highlighting the rupee's real effective exchange rate sits near 89.7 (as of 8th June, the time of recording), about 10% below its ten-year average, and the lowest since the 2013 Taper Tantrum.

Think of the rupee's "real effective exchange rate" (REER) as a fair-value score for the currency pegged to the USD. When the score is high, the rupee is expensive compared to its trading partners. When it's low, the rupee is considered underpriced. Right now that score sits near 89.7, roughly 10% below its ten-year average. The last time it was this low was 2013, which saw the rupee recover.

Ashish pointed out that the rupee is cheaper than it has been in over a decade.

Ashish believed the rupee is unusually undervalued, and that this could be an opportunity for foreign investors with a 3–5 year horizon.

His point was that the rupee's weakness looked more like a temporary flow issue than a problem with India's fundamentals. Global capital could start rotating back into India, oil prices soften, and RBI/government measures support inflows, the rupee could recover.

So for investors entering now, the opportunity may not just be Indian market returns. There could also be a second layer of return if the INR strengthens over time.

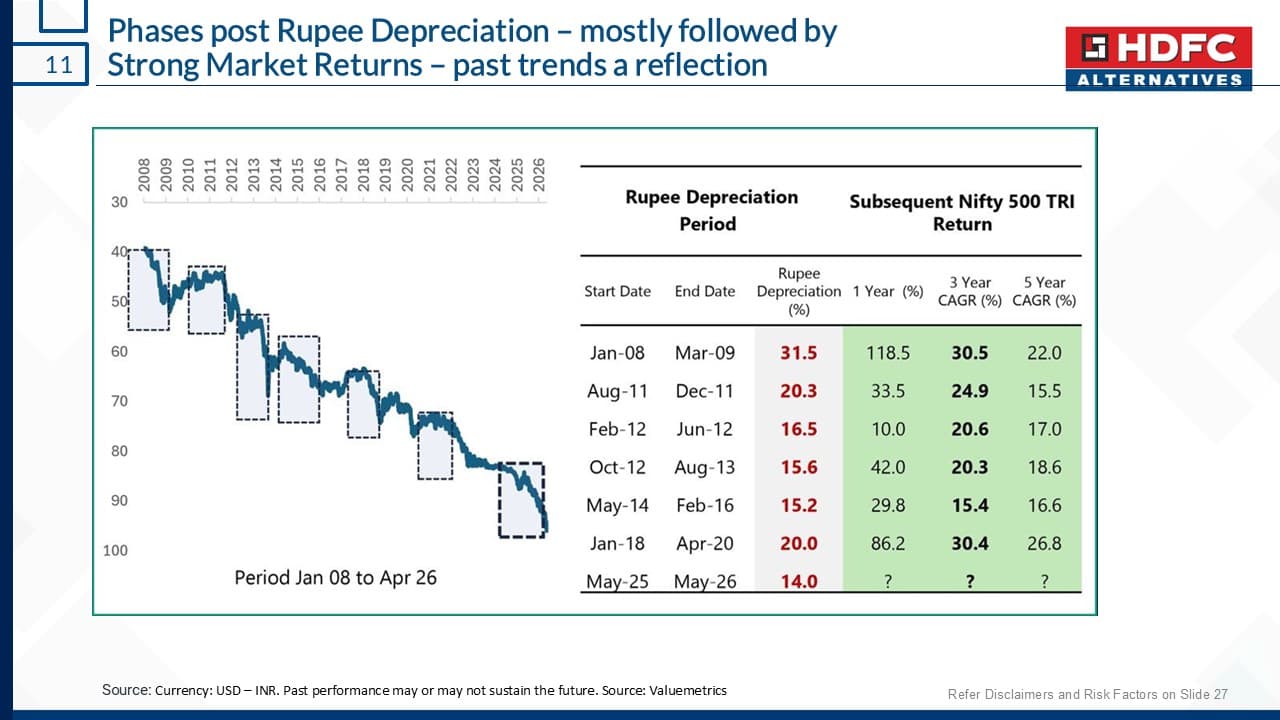

Ashish also shared insightful data on how Indian markets have always bounced back very strongly after a year of INR depreciation. He did however highlight that past performance isn't a guarantee of future performance.

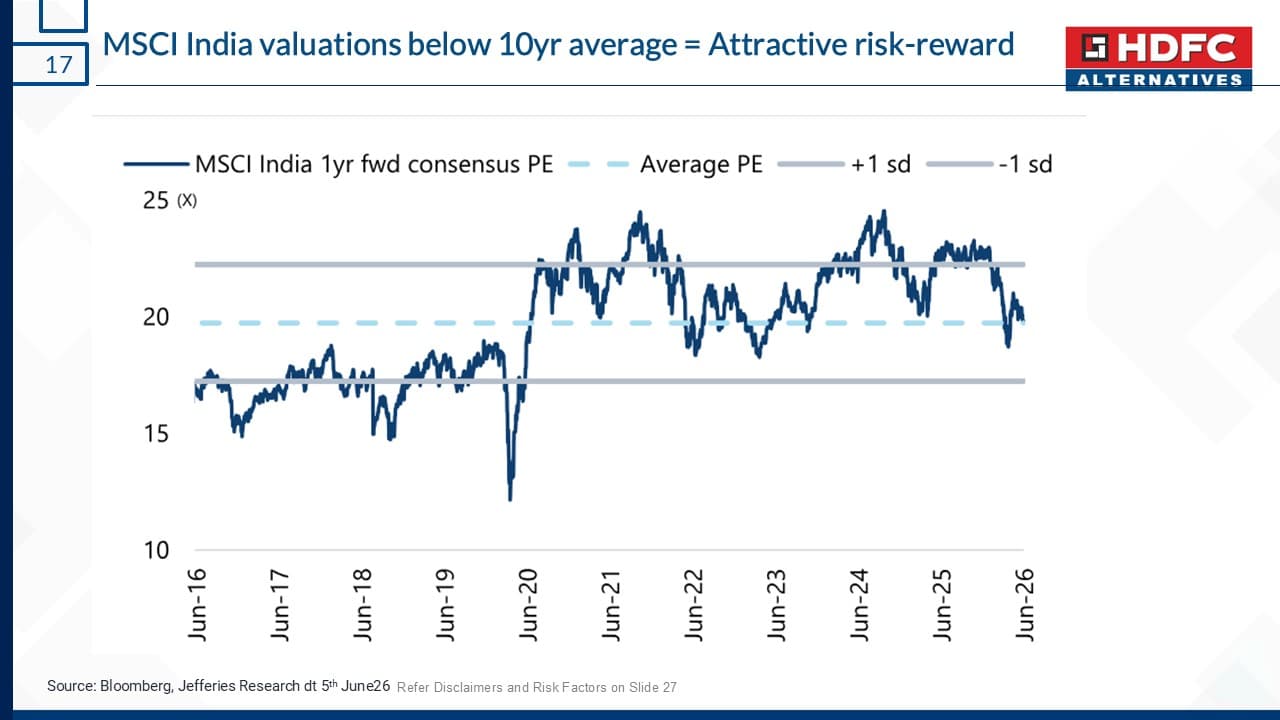

Q2) Is India Overpriced?

Not right now, Ashish believes. He pointed to the MSCI India index, basically a basket of India's largest listed companies that global investors use as a yardstick for how expensive or cheap the market is.

Right now that yardstick is trading below its ten-year average valuation following the recent correction. In his view, the "India premium" most people assume they're paying simply isn't there at the moment.

He also sees a structural change that gets overlooked: the market has a new shock absorber. Indian households now invest roughly US$4 billion every month through SIPs, steady domestic flows that, he noted, have repeatedly cushioned periods of foreign selling. To his eye, it's a different market from the one that used to lurch every time overseas investors headed for the exit.

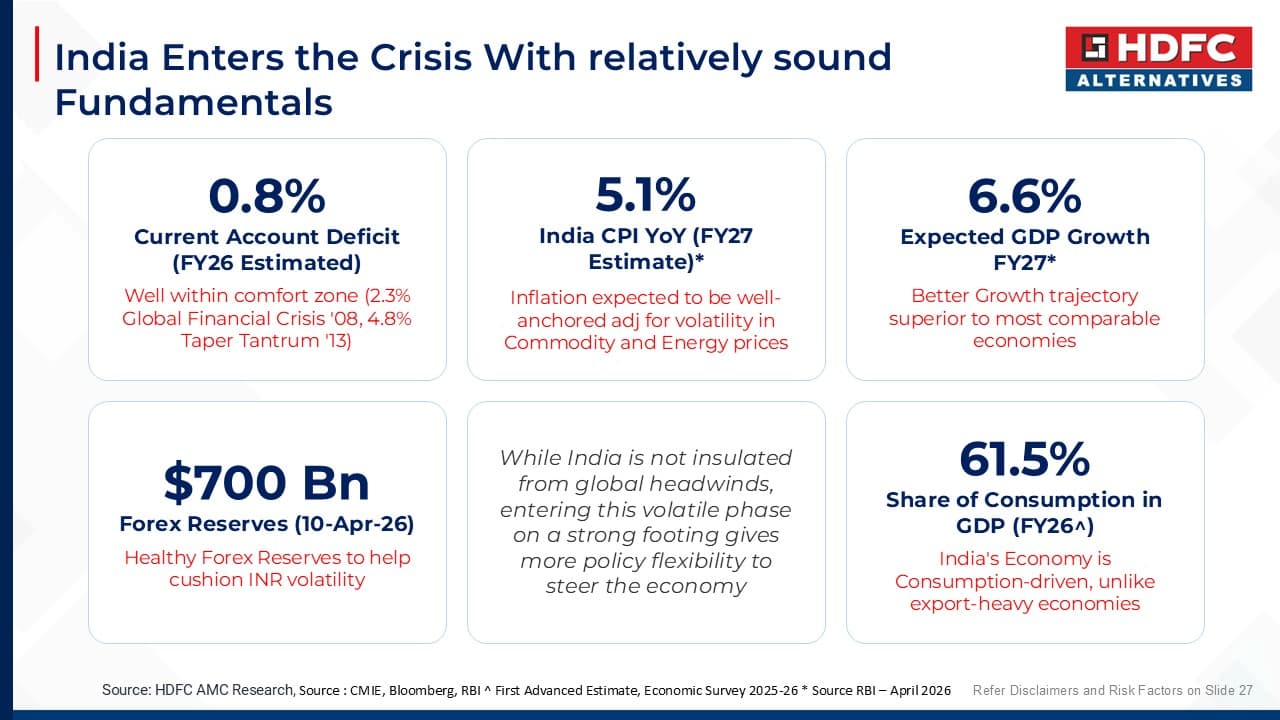

Q3) How Risky Is The World Right Now?

US–Iran tensions, energy risk around the Strait of Hormuz, global risk-off flows, all of it was addressed in the webinar.

Ashish's view was measured: India is not immune to global shocks, but it enters this period with stronger fundamentals than in most past crises and a far deeper base of domestic investors to lean on. This was backed up by relevant data on India's fundamentals.

Q4) What About Tax?

The answer splits in two.

This is the question that best shows why your needs are specific, right down to the country, and was taken by Indus CEO, Jai Goradia.

If you're in New Zealand, the India–New Zealand tax treaty (DTAA) means you don't pay Indian tax on your mutual fund returns. Indus automates availing of the treaty on your behalf, so you receive your full return at the click of a button. You may be liable for FIF for investments over $50,000.

If you're in Australia, DTAA benefit applies differently. India handles your India taxation by deducting the applicable TDS, which is reflected when you sell a mutual fund on the Indus app, completely automated for you. You can request a tax statement and use that to potentially claim a foreign tax credit in Australia, depending on your circumstances.

Important Information: Indus does not provide tax advice and we recommend seeing an independent tax advisor to understand your obligations.

The Most Compelling Takeaway

Near the end, Ashish said something several attendees grabbed a screenshot of:

"The people who benefit from market cycles are usually not the ones who predict every crisis correctly. They're the ones who stay invested through cycles, with the right time horizon."

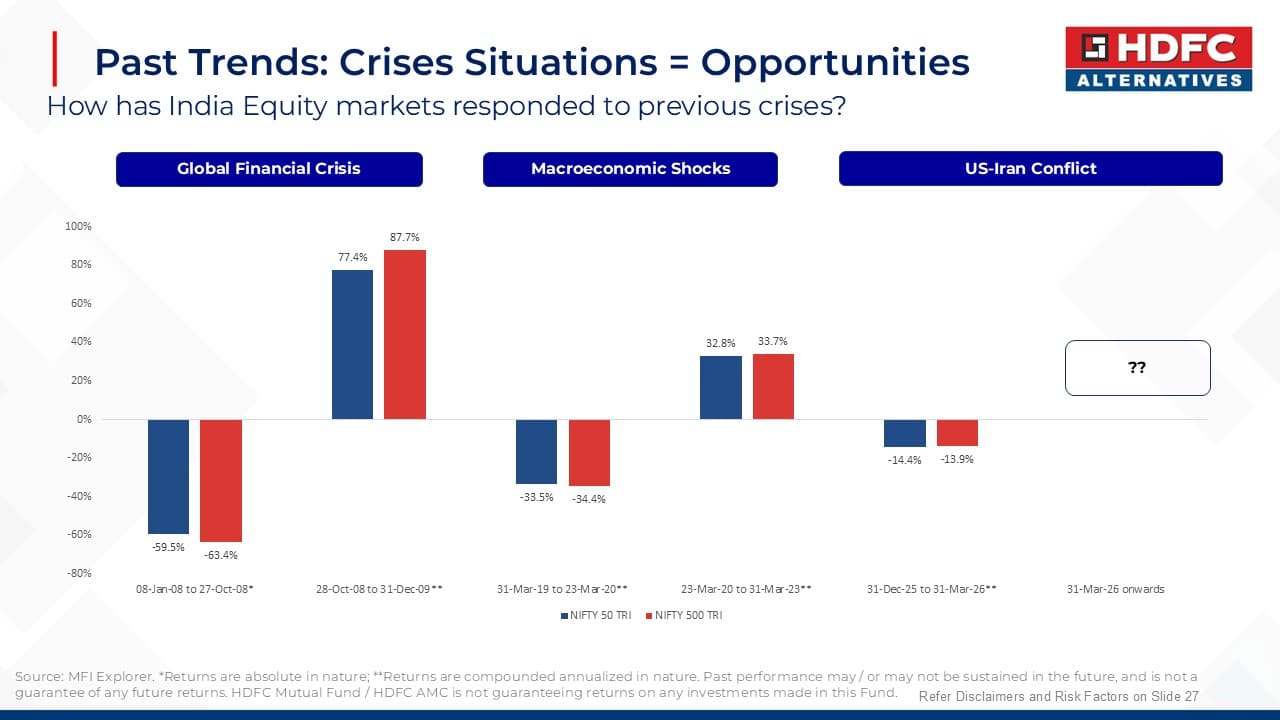

Crises have historically created opportunities. Timing them has historically humbled everyone.

He highlighted the potential upside growth and pointed to the robustness of the Indian market, highlighting the Indian market's uncanny ability to bounce back strongly after every crisis.

Conclusion

If there was one thread running through every answer, it was this: India is worth looking at right now, but only with the right time horizon and the right context for where you actually live.

The rupee may be a tailwind rather than a drag. Valuations aren't carrying the premium most people assume. The world isn't calm, but India enters this stretch with deeper domestic support than it's had in past crises.

At Indus, we are dedicated to continuing to bring you direct access to our partners and enable fund managers like Mr. Ashish Jagnani to take your most pertinent questions.

Disclaimer:

This blog is general information only and does not take into account your objectives, financial situation, or needs. It is not personal financial, investment, or tax advice, and should not be relied on as such. Before acting on anything here, consider whether it is appropriate for you and seek advice from a licensed financial adviser and an independent tax adviser.

Investing carries risk, including the possible loss of capital. The value of investments can rise and fall. Past performance is not a reliable indicator of future performance, and any figures, valuations, or exchange rates mentioned were accurate as of the webinar date and will change over time. Currency movements can increase or reduce returns for international investments.

Tax outcomes depend on your individual circumstances and country of residence, including obligations such as FIF rules in New Zealand and foreign tax credits in Australia. Indus does not provide tax advice. Please consult an independent tax adviser to understand your obligations.